Market Update – June 2024

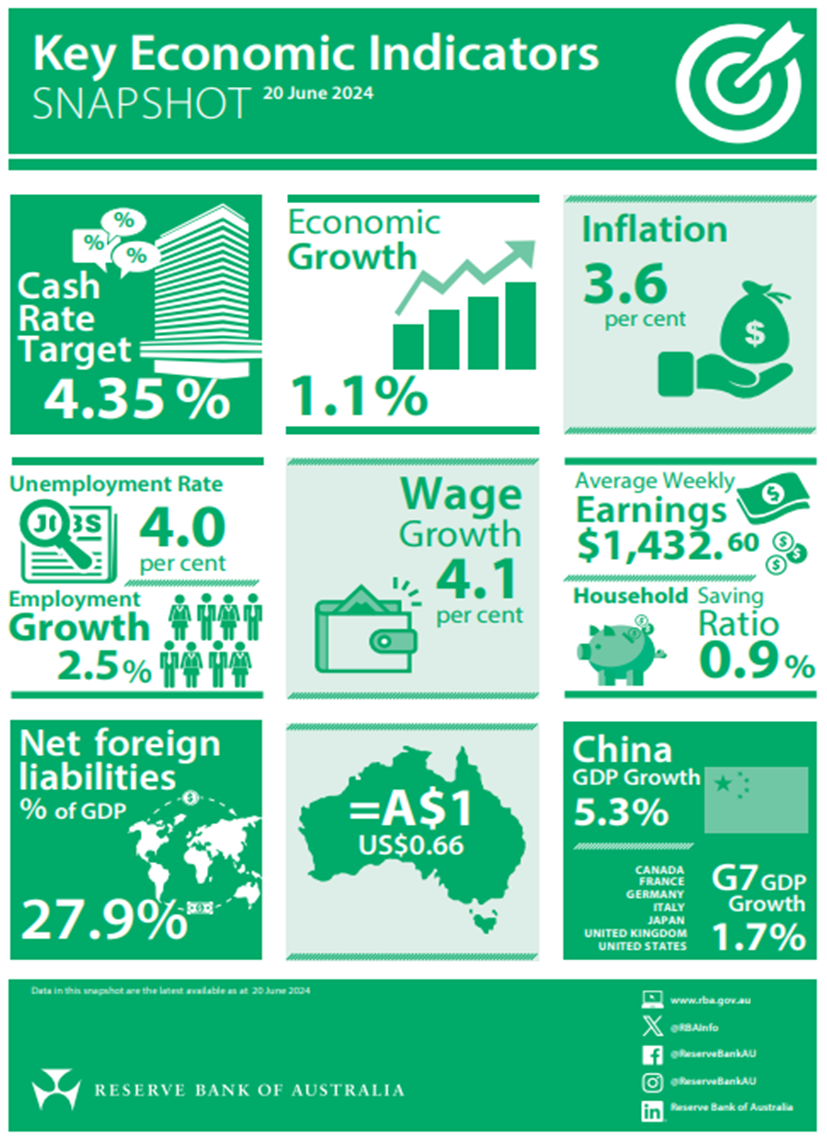

- Inflation and Interest Rates: The Reserve Bank of Australia (RBA) maintained the cash rate at 4.35% in June. The annual inflation rate eased to 3.6%, down from 4.1% in May, driven by lower energy and food prices. However, services inflation remained high due to tight labor market conditions, indicating ongoing wage growth and employment strength.

- Equity Market: The ASX 200 index rose by 1.7% in June, buoyed by gains in the financial and mining sectors. The index closed at 7,796 points, with an average for the month of 7,822 points. Financials benefited from higher interest margins, while the mining sector experienced robust demand for key exports like iron ore. Despite these gains, investor sentiment was cautious due to potential future rate hikes and global economic uncertainties.

- Economic Performance: Australia’s GDP growth remained stable at an annualized rate of 1.7%. The unemployment rate stayed low at 3.5%, indicating a tight labor market supporting wage growth. Consumer confidence showed a slight improvement but remained subdued due to concerns over household debt and living costs.

Sector Analysis:

- Financial Sector: The Australian financial sector saw significant growth due to higher interest margins and increased lending activities. Major banks reported strong quarterly earnings, contributing to the overall positive performance of the ASX 200 index.

- Mining Sector: The mining sector continued to benefit from strong global demand for commodities such as iron ore and lithium. Australia’s position as a leading exporter of these key resources bolstered the sector’s performance, with mining companies reporting higher revenues and profits.

US Market

Economic Indicators and Performance:

- Earnings Growth: U.S. equity markets continued their upward trajectory, driven by robust earnings growth, particularly in the technology sector. The S&P 500 index increased by nearly 5% in June, bringing the year-to-date return to 11.3%. Major technology companies, such as Nvidia, saw substantial earnings revisions, which further boosted market performance.

- Federal Reserve Policy: The Federal Reserve held the federal funds rate steady at 5.25% – 5.5%. The Fed signalled potential rate cuts later in the year, contingent on inflation and economic growth trends. Inflation in the U.S. moderated to the 3%-4% range, providing some relief and supporting equity valuations. However, the Fed remained cautious, indicating that rates could stay higher for longer if inflationary pressures persist.

- Economic Performance: The U.S. GDP grew at an annualized rate of 2.0% in Q1 2024. The unemployment rate stood at 3.6%, reflecting continued labor market strength. Consumer spending showed signs of slowing as high interest rates impacted household budgets, particularly in interest-rate-sensitive sectors like housing and consumer goods.

Sector Analysis:

- Technology Sector: The technology sector was the standout performer, driven by strong earnings and investor enthusiasm for AI-related stocks. Companies like Nvidia and Alphabet reported significant earnings growth, contributing to the sector’s robust performance.

- Healthcare Sector: The healthcare sector also performed well, supported by innovation in pharmaceuticals and biotechnology. Companies developing new treatments for chronic diseases saw increased investor interest and stock price gains.

European Market

Economic Indicators and Performance:

- Monetary Policy and Valuations: European equity markets remained stable, supported by the European Central Bank’s (ECB) early monetary easing. The ECB’s dovish stance helped maintain attractive valuations, though earnings growth was slower compared to the U.S. The ECB’s policy adjustments aimed to balance growth support with inflation control, which stood at 3.5%.

- Sector Performance: Sectors such as green energy received increased attention due to potential regulatory changes influenced by upcoming elections. The broader market sentiment was positive, bolstered by improving economic indicators and supportive fiscal policies designed to stimulate growth.

- Economic Performance: The Eurozone’s GDP grew at an annualized rate of 1.2% for Q1 2024. Inflation moderated to 3.5%, allowing the ECB to maintain its supportive stance. Unemployment remained at a historic low of 6.5%, which supported consumer confidence and spending, particularly in sectors like retail and services.

Sector Analysis:

- Green Energy Sector: The green energy sector saw increased investment and stock price appreciation, driven by government initiatives and regulatory support for renewable energy projects. Companies involved in solar, wind, and battery storage technologies benefited from these trends.

- Industrial Sector: The industrial sector experienced steady growth, supported by strong export demand and investment in infrastructure projects across the Eurozone. Companies involved in construction, engineering, and manufacturing reported positive earnings growth.

Asian Market

Economic Indicators and Performance:

- Japanese Equities: Japanese equities saw moderate gains, driven by increasing domestic demand and a stable yen. The Nikkei 225 index rose by 2.3% in June, reflecting investor optimism about economic recovery and corporate earnings growth. The Bank of Japan’s supportive monetary policy and positive economic indicators contributed to this performance.

- Chinese Equities: The Chinese equity market faced challenges as momentum waned due to long-term issues in the export and manufacturing sectors. Investors remained cautious amid uncertain monetary policy support and expectations of increased government fiscal spending to boost economic growth.

Sector Analysis:

- Technology Sector: The Japanese technology sector benefited from strong demand for electronic components and advanced manufacturing equipment. Companies involved in semiconductor production and robotics saw increased investor interest.

- Consumer Goods Sector: The consumer goods sector in China faced headwinds due to slower economic growth and declining export demand. However, domestic consumption remained relatively stable, providing some support to the sector.

Commodities and Currencies

- Oil and Metals: Oil prices remained stable due to balanced supply and demand dynamics. Industrial metals experienced a price spike driven by speculation on limited supply, which is expected to stabilize as production adjusts to higher prices. This stability in commodity prices provided some relief to inflationary pressures globally.

- Gold and USD: Gold prices increased in anticipation of global monetary policy easing. However, potential delays in Fed rate cuts could lead to a near-term correction in gold prices. The U.S. dollar is expected to remain stable over the summer, supported by relatively higher U.S. economic growth and interest rates compared to other major economies.

Commodity Market Analysis:

- Energy Sector: The energy sector saw mixed performance, with stable oil prices but increased volatility in natural gas markets. Geopolitical tensions and production adjustments by OPEC+ influenced market dynamics.

- Precious Metals: The precious metals market experienced increased investor interest, with gold and silver prices rising due to economic uncertainty and inflation concerns. Investors sought safe-haven assets to hedge against potential market volatility.

Conclusion

June 2024 saw mixed performance across global equity markets. Strong earnings growth, particularly in the technology sector, drove U.S. markets higher, while European and Asian markets displayed more modest gains influenced by regional economic conditions and central bank policies. As the year progresses, investors will closely monitor economic data and policy decisions to navigate the evolving market landscape and identify growth opportunities. The focus will remain on central bank actions, inflation trends, and geopolitical developments as key determinants of market performance.

Future Outlook on Global and Australian Interest Rates

As we progress into the latter half of 2024, several key factors are expected to shape the trajectory of global interest rates:

Monetary Policy Adjustments:

Federal Reserve (U.S.): The Federal Reserve is anticipated to maintain a cautious approach regarding interest rate cuts. While there is potential for rate reductions later in 2024, the exact timing will depend on inflation trends and economic performance. Current projections suggest a gradual decrease in the federal funds rate, potentially dropping to around 4.25% by the end of 2024 if inflation continues to moderate.

European Central Bank (ECB): The ECB is likely to continue its accommodative stance, balancing efforts to support economic growth with the need to control inflation. With inflation in the Eurozone moderating to around 3.5%, the ECB might consider slight rate reductions but will proceed cautiously to avoid economic overheating.

Bank of Japan (BOJ): The BOJ is expected to maintain its ultra-loose monetary policy to support economic recovery and boost inflation towards its 2% target. Given the persistent low inflation and economic challenges, significant rate hikes are unlikely in the near term.

Inflation Trends

Global inflation is expected to continue its downward trend, influenced by stabilizing commodity prices, easing supply chain disruptions, and moderated demand. However, regional variations will persist, with advanced economies experiencing more stable inflation rates compared to emerging markets.

Geopolitical Risks and Economic Uncertainty:

Geopolitical tensions, particularly in regions like the Middle East and Eastern Europe, could impact global supply chains and commodity prices, thereby influencing inflation and interest rate decisions. Central banks will remain vigilant and responsive to these external shocks.

Technological Advancements:

The integration of advanced technologies such as artificial intelligence (AI) and automation could lead to productivity gains, potentially easing inflationary pressures in the long term. However, the initial capital expenditure required for these technologies might create short-term inflationary spikes.

Australian Interest Rates Outlook

For Australia, the outlook for interest rates is influenced by both domestic economic conditions and global economic trends:

Reserve Bank of Australia (RBA) Policy:

The RBA is projected to maintain a relatively high cash rate at 4.35% through the end of 2024, reflecting ongoing concerns about inflation, which stood at 3.6% in June year over year. However, if inflation continues to decrease, the RBA may consider rate cuts in early 2025. The central bank’s decisions will be data-dependent, closely monitoring inflation, wage growth, and economic activity.

Inflation and Economic Growth:

Inflation in Australia is expected to moderate gradually, supported by stabilizing energy and food prices. The RBA aims to bring inflation within its target range of 2-3%. Economic growth is projected to remain stable at around 2.3% annually, supported by strong performances in the financial and mining sectors.

Wage growth, driven by a tight labor market, could create upward pressure on inflation, potentially delaying significant rate cuts.

Housing Market and Consumer Spending:

High interest rates have impacted the housing market, with slower growth in property prices and reduced affordability. The RBA will likely consider the housing market’s health when making future rate decisions.

Consumer spending, which has shown signs of slowing due to high interest rates, will be a critical factor. The RBA will aim to balance the need to control inflation with the desire to support consumer spending and overall economic growth.

Global Economic Influence:

Australia’s interest rate decisions will also be influenced by global economic trends, particularly in major trading partners like China and the United States. Any significant changes in the economic policies of these countries could impact Australia’s trade dynamics, inflation, and economic growth, thereby influencing the RBA’s monetary policy stance.

Advice Warnings & Disclaimers.

This information is intended to provide general information only and has been prepared without considering any particular person’s objectives, financial situation or needs. Any general advice contained within or given during this presentation (whether orally or in writing) does not consider your objectives, financial situation or needs. Nothing in this presentation is intended to be investment, financial advice or a recommendation to invest in a financial product. Before acting on such information, you should consider the appropriateness of the information having regard to your personal objectives, financial situation or needs. To the maximum extent permitted by law, we (Forward Path Advisory Pty Ltd), Joel Cleary & Rathakrishna Jeyabalasingam (Rads Je) disclaim all liability and responsibility for any direct or indirect loss or damage which may be suffered as a result of relying on anything in this podcast, including any forward-looking statements. Past performance is not an indication of future performance. In particular, you should obtain professional advice before acting on the information contained in this presentation.